Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Growers who choose to store their cotton and wait for high prices may want to consider a common hedging strategy.

The 2023 cotton crop has been challenging in many ways. Across Texas, the ’23 crop was not the booming recovery that growers needed to make up for the drought disaster in 2022. In some situations, the ’23 crop was as bad or worse than 2022.

From a price standpoint, ICE cotton futures have been rangebound, bouncing off repeated attempts to breach 90 cents. The U.S. physical market has been relatively slow and inactive because the available foreign export demand appears to be consuming the ample Brazilian and Australian supplies first. That means that it is likely that unbought U.S. bales will spend some months in storage. Growers who choose to store and wait for higher prices will end up having associated storage costs built into their cash bids. What to do?

A common hedging strategy may apply to this situation. Growers can sell soon after harvest and then buy call options on an underlying ICE cotton futures contract. This avoids or minimizes storage costs, and it eliminates downside price risk. However, this strategy preserves upside pricing opportunity.

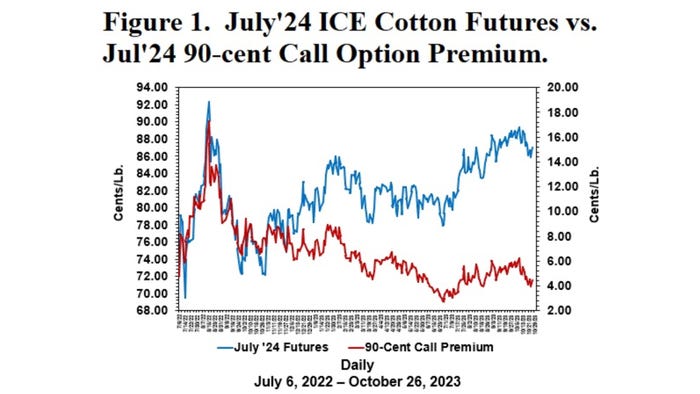

Call options premiums (the red line below in Figure 1) increase in value with increases in the futures market price (the blue line in Figure 1). This is because the owner of a call option has the right, but not the obligation, to have bought the futures market at the call strike price. For example, in Figure 1, the red line represents the value of owning the right to have bought July ’24 futures at 90 cents.

Such a position would have “intrinsic” value (i.e., in a buy-low, sell-high sense) if July ’24 futures traded above 90 cents. This value is partially reflected by the rising premium (the red line in Figure 1) when the underlying futures price is also rising (the blue line).

Call option hedging strategies make sense when combined with cotton that was been cash-contracted. For example, suppose a grower sells his 2023 bales for current cash prices, but is worried about missing out on higher prices. Having sold his physical cotton, he is no longer concerned about storage or declining prices. His remaining concern may be missing out on higher prices. A 90-strike July '24 call option costs 4.45 cents per pound as of Oct. 26. That is the up-front insurance premium the grower would pay to insure against missing out on a rally in July '24 futures.

When should growers consider such a strategy? The first answer involves your market opinion. If you think there is a limited chance of higher prices in the spring, then it wouldn’t make sense to either store or buy call options. Just sell now.

But if growers think that prices might be higher in the future, then perhaps they should consider either storing or buying calls. The relevant question then is whether the premiums paid for call options are cheaper than the costs of storage. Paying for storage buys you time. Paying for call options buys you time. Which one is cheaper is a math question. All I can say is that the low volatility of the rangebound pattern of ICE futures has cheapened up option premiums relative to the past, so maybe it is worth looking into.

Another question that growers may ask is “Will call option strategies pay?” The answer is, of course, unknown. It’s an insurance purchase, not a government program. Do you really care if your homeowner’s policy pays off? Or your auto insurance? The more relevant insurance questions are, as always, what coverage you are getting and at what price.

So far this season, the July '24 contract hasn't had a major rally (implying this is insurance that has not paid off). A cheaper version of this strategy would be to buy 90 calls on earlier spring contracts, i.e., March '24 or May '24. Call option strategies can also be cheapened up by implementing them as call spreads (buying a lower strike call and selling a higher strike call).

In summary, owning a call option represents insurance against selling your cash cotton and then missing out on a later price rally. It is also a substitute/compensation for storing your cotton for later cash sale (or for putting it in the CCC loan for later sale).

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/.

You May Also Like

Enter a zip code to see the weather conditions for a different location.