Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Lower-than-expected soybean stocks estimate suggests the 2022 U.S. soybean crop may be overestimated.

The March 31 USDA Grain Stocks and Prospective Plantings reports were bullish for soybeans, supportive for old-crop corn, but bearish for new-crop corn.

As highlighted in recent writings, the potential for significant (and unpredictable) price swings exists with the release of the USDA Prospective Plantings and Grain Stocks reports and more surprises were seen this year.

Starting with beans, the USDA pegged March 1 stocks at 1.685 bbu, which was sharply below the average trade estimate of 1.728. Early ideas are that the lower-than-expected stocks total implies that the USDA overestimated the 2022 U.S. soybean crop.

Any adjustment to crop size has historically not been made until the September Grain Stocks report, although USDA may elect to increase its estimate of residual use in the April 11 WASDE report. That could lead to an ending stocks estimate for 22/23 below 200 million bushels.

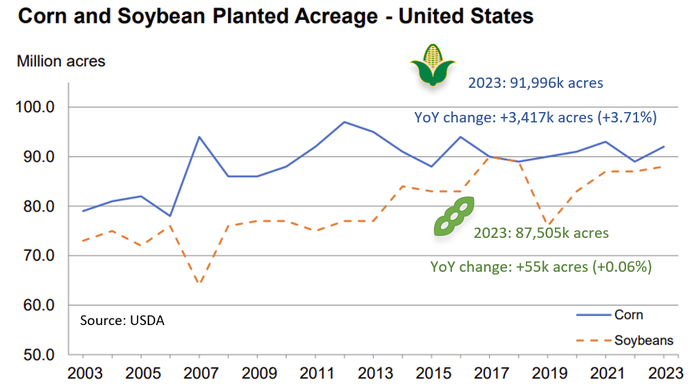

The Prospective Plantings report pegged 2023 acreage at 87.5 million, which was 0.8 million below the average trade estimate of 88.3 (range 87.4-89.6) and only fractionally higher than 2022. Utilizing the trend yield from the USDA Outlook Forum of 52.0 bushels per acre, production would be 4.5 billion bushels. After incorporating the aforementioned reduction in beginning stocks and utilizing usage estimates from the Outlook Forum, ending stocks for 2023/24 could fall below 250 mbu.

Turning to corn, the Grain Stocks report pegged March 1 inventories at 7.401 bbu—73 mbu below the average trade estimate of 7.474 (range 7.240-7.830). Friday’s report confirmed that total feed usage from September through February was around 3.82 bbu, or 7% below a year ago. The current USDA forecast of annual feed use for 22/23 is nearly 8% lower.

However, given the narrowing wheat-corn spread, significant substitution of wheat for corn is possible in feed rations this summer. This suggests that a notable change in annual corn feed use is unlikely in the April 11 supply/demand report.

Turning to the Prospective Plantings report, the USDA estimated 2023 acreage at 92.0 million acres. That was 3.4 million acres higher than last year, above the average trade estimate of 91.0 million and near the top end of the range of 87.7-92.1.

Utilizing the USDA trend yield from the Ag Outlook Forum of 181.5 bpa, production for 2023 would be a record 15.248 bbu. Incorporating the current USDA ending stocks projection for 2022/23 of 1.342 bbu and adding in a small amount of imports, total supply for 2023/24 would be 16.6 bbu. Usage for 2023/24 from the Outlook Forum was 14.5 bbu.

Under these assumptions, ending stocks for 2023/24 would increase to 2.1 bbu, which would be an increase of more than 50% from the current year and the highest level in five years.

A bullish reaction to the reports was seen for soybeans as expected, while new-crop corn posted slight declines. Given the uncertainty on weather associated with the spring planting season, the potential for increased price volatility is high.

It remains critical to maintain close contact with your Advance Trading advisor and execute risk management strategies to defend your balance sheet. Contact Advance Trading at (800) 747-9021 or go to www.advance-trading.com.

Information provided may include opinions of the author and is subject to the following disclosures:

The risk of trading futures and options can be substantial. All information, publications, and material used and distributed by Advance Trading Inc. shall be construed as a solicitation. ATI does not maintain an independent research department as defined in CFTC Regulation 1.71. Information obtained from third-party sources is believed to be reliable, but its accuracy is not guaranteed by Advance Trading Inc. Past performance is not necessarily indicative of future results.

The opinions of the author are not necessarily those of Farm Futures or Farm Progress.

You May Also Like

Enter a zip code to see the weather conditions for a different location.