Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

November 14, 2023

By Kenny Burdine, University of Kentucky

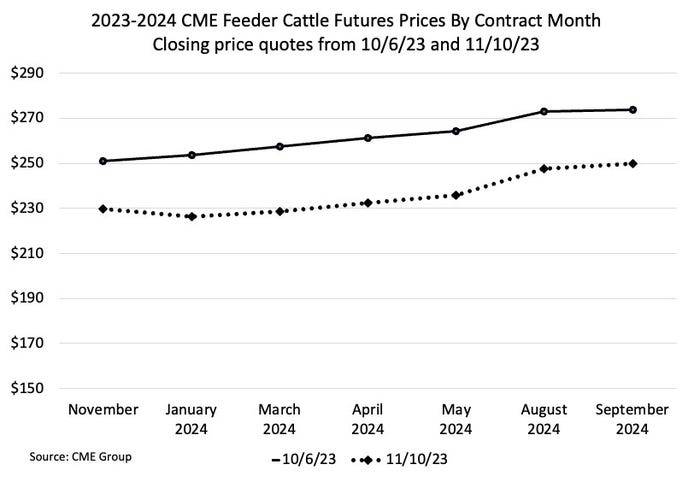

Feeder cattle prices have been trending down since mid-September and last week was especially frustrating for cattle producers. As I write this on the afternoon of Nov. 13, CME© feeder cattle futures are down $30-$40 per cwt from their September highs, depending on the contract month one is looking at.

Cash feeder cattle prices have fallen during this time, but not by as much. Here in Kentucky, there also seems to be a lot of variation in local price levels, which suggests that markets have gotten pickier over the last several weeks. A full week of sales this week should tell us more as the markets process everything that has occurred recently.

While not scientific, it has been my observation that it is hard to build much momentum in feeder cattle markets this time of year. Prices tend to decline seasonally during fall, and the markets seem to seize negative news because of that. Swings in weather and temperatures, along with increased health issues as we move towards winter, don’t help either. There has been some negative “new information” for markets to digest, but the response has been larger than I would have expected.

I want to make it clear that the longer-term supply fundamentals still look good. But there have been lingering questions on the demand side of the equation: inflation, interest rates, consumer debt levels, etc. The war in the middle east was something new the market had to process on top of everything else and I think this had an impact the last few weeks. At the same time, there have been two recent USDA reports that were also bearish.

Last month, the October Cattle-on-Feed report came in with much higher September placements than expected. I chalked this up to weather and thought it was more a question of timing of when cattle were moved into feedlots. I didn’t expect high placement levels to persist through the end of the year because I didn’t think there were that many feeder cattle outside of feedlots. But the pre-report estimates for this Friday’s November Cattle-on-Feed report suggest October may have been another large placement month. Josh will write about the November report next week when we know what the actual numbers look like.

Last Thursday was a tough day on the board and it appears that we have only gained about one-third of that decrease back between Friday’s trade and what I am seeing today. The main piece of new news Thursday was the November WASDE.

Grain crops are typically the focus of this monthly supply / demand report from USDA, but it also includes estimates for meat production. This part of the report is not usually a major cattle market mover, but it sure had an impact last week. USDA raised their beef production forecast for 2024 by about 2% from the October estimate, which would be very significant. Undoubtedly, this is related to higher placements this fall. A production increase of that amount lowers the expectation of fed cattle prices next year and that gets reflected in feeder cattle values.

If we are honest with ourselves, this cattle market had been on a run since spring and probably had gotten a little over-heated. I don’t think anyone would have been shocked by a downward correction, but the magnitude of the drop over the last couple of months has been more than most would have guessed. The good news is that the overall supply picture is encouraging – cow numbers are low and getting lower. So, calf crops are likely to keep getting smaller for a couple years.

I’m guessing people get tired of me saying things like this, but this is also a reminder of the importance of risk management. In a world where our price risk management tools are market-based, when markets change, those pricing opportunities disappear. So, it is important that producers be proactive about managing price risk, just like any other risk to their operation.

Read more about:

Market ReportsYou May Also Like

Enter a zip code to see the weather conditions for a different location.