Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Calculating your ability to purchase farmland.

A goal of many pursuing the American dream is home ownership. Similarly, the goal of a farmer is often to become a landowner. Like buying a home, the financial decision to purchase farmland is clouded by emotional, social, and familial influences.

How can a farmer clearly evaluate their financial position to purchase farmland when these influences are at play? The answer is, going back to the basics – analyzing the numbers.

Most farmers will seek financing to complete a farmland purchase, and it’s important to have an idea of your purchasing position before you approach lenders. There are two important angles when it comes to considering cash requirements for a land purchase:

Cash needed immediately for a down payment (and/or land and building improvements)

Recurring annual cash flow needed to make the farm loan payment.

Depending on the size of the farm, a high purchase price per acre will result in a substantial chunk of cash needed for a down payment.

In some instances, buildings in disrepair, nutrient depleted soil, and/or a neglected water mitigation (or irrigation) system may create additional upfront cash requirements. Also remember to plan for soft costs like surveying, appraising, and bank fees that will increase either your down payment or your total loan amount.

Healthy working capital and a current ratio of 1.5 or greater are good indicators of cash availability (liquidity), and it is important to consider the status of your remaining liquidity after making a down payment.

Many lenders will require a 15-20% down payment on quality farmland, and subpar land may require an even larger down payment. There are programs that exist for beginning farmers that require as low as a 5% down payment.

If you don’t have the cash available, you may consider accessing equity in other assets. Keep in mind, the smaller the down payment, the larger the loan payment each year. Many lenders may offer a lower interest rate for a larger down payment upfront.

As the source of the down payment is being solidified, a concurring step should be calculating the loan payment amount and how it will impact your future cash flow. This can be intimidating if you aren’t a numbers person, but it’s powerful information to know before you begin meeting with lenders.

A simple Google search will yield multiple tools to calculate a loan payment. Specifically, limiting the search to a “farmland” loan calculator will result in a semi-annual or annual payment option, the most common payment structures for farmland loans.

Understanding the payment options and financing structure will position the farmer to better negotiate terms, and plan for the impact on cash flow.

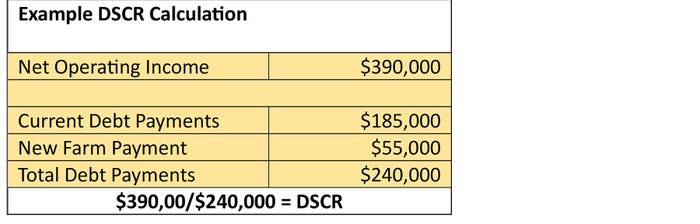

Lenders want to see that the operation can pay back the money loaned to the farm. They will often use a ratio called a Debt Service Coverage Ratio (DSCR) as one tool to determine the repayment capacity of the farm. This ratio compares the Net Operating Income, or cash you have available to make your debt payments, to existing debt payments and the new loan payment.

Learning how to calculate the DSCR yourself can be a great way to determine your purchase power.

There isn’t a firm financial standard for DSCR. A DSCR of 2.0 or more is considered very strong, and a DSCR of less than 1.0 means there isn’t enough income to make debt payments. Many lenders set a threshold of 1.2 or 1.25 as a minimum requirement.

This is one of the most basic calculations to determine repayment capacity, but it isn’t perfect. It can vary widely from year to year, as it starts with Net Farm Income – which we know is volatile!

For a more thorough understanding, also calculate the five-year average of net operating income and debt payments.

If you’re buying a farm that you are paying rent for, recognize that your net farm income will increase by that rent amount, and you’ll have it available to apply towards the debt payment.

If the farm to be purchased is new ground, include a projection of crop or livestock revenue & expenses that the farm will generate in your calculation. There needs to be enough money left after your debt payments to fund any family living requirements and satisfy your tax liabilities, so don’t forget to include those figures – and be realistic about the family living number!

Even if you aren’t actively looking to purchase a farm, understanding your debt capacity is important in managing your farming operation. This process can be applied to other purchases as well, like building grain bins or purchasing equipment.

An unexpected death or life change in your area may present an opportunity to purchase land, equipment, or buildings.

If you know your financial position, you can evaluate clearly whether the deal is a good one, outside of the emotions involved. Is the land good quality? Is the equipment in good shape? Is it truly a good financial decision for my farming operation?

Knowing that you can afford a purchase creates room for you to consider the other details. As always, talking with trusted professionals like your accountant, financial advisor, tax preparer, and banker can help you understand your financial position.

Source: Southern Ag Today

You May Also Like

Enter a zip code to see the weather conditions for a different location.