Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Financial Outlook: The Federal Reserve kept interest rates unchanged on Wednesday. What that – and other economic indicators and consumer trends – means for farmers and their families.

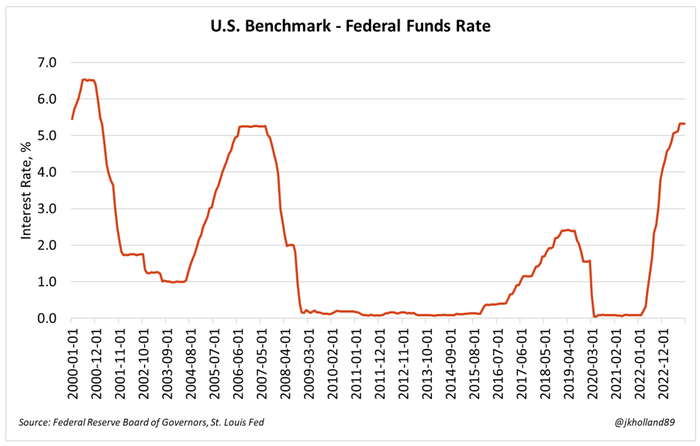

The Federal Reserve left interest rates unchanged yesterday following the conclusion of its two-day Federal Open Market Committee meeting. Rates continue to hover between 5.25% and 5.5% – a 22-year high.

I heard an interesting anecdote from my husband yesterday, who works in healthcare construction. He was talking with a real estate developer friend of his earlier this week who has been grappling with several customers who are backing out of deals recently.

Their reasoning? They can make more returns by putting their money into T-bills than they can on increasing rents on their clients.

And while my husband’s friend didn’t say this explicitly, I also pointed out to Chris that investors really aren’t that interested in stocks right now – the return on Treasury notes is so strong that investors would rather place their money in those assets instead of betting on risker and likely lower returns from the stock market or even private equity.

How does this relate to yesterday’s FOMC meeting? Despite higher inflation readings posted earlier this fall, the rising Treasury note yield is one of the clearest signals to date that the economy may finally be cooling off.

That’s not to say we are going to see interest rates cool off anytime soon. While the recent activity in the bond market reduced the likelihood that the Fed will increase interest rates once more next month, the chances that the Fed will keep current interest rates in place remain high.

“Fed officials believe that the run-up in long-term rates will effectively do some of their work for them in restraining the economy, and are heartened by how inflation, while still too high, has cooled over the past year,” Justin Lahart of the Wall Street Journal wrote this morning. “But if inflation does reaccelerate, they are ready to tighten more.”

It’s cautious optimism, but it’s optimism, nonetheless.

Bond yields drifted higher this morning, closing in on the 4.7% benchmark. S&P 500 stocks rallied yesterday following the Fed’s post-FOMC meeting conference and continued 0.68% higher this morning to $4,284.75 as yesterday’s optimism spilled over into the early morning trading session.

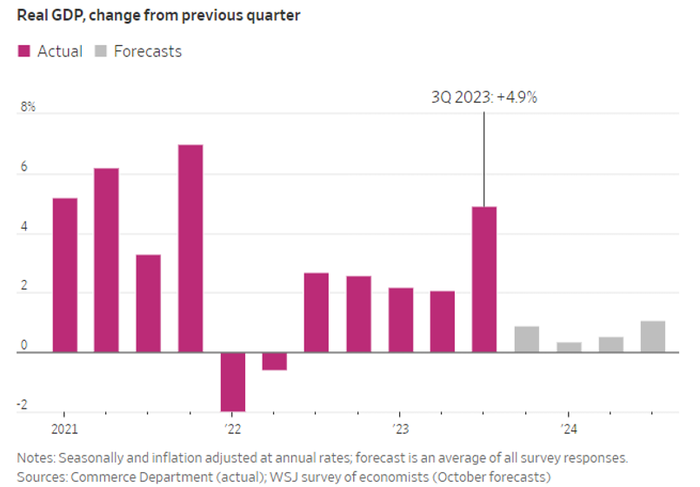

Last week’s gross domestic product report showed that third quarter economic growth was posted at 4.9% - over double the previous quarter’s growth rate and the highest growth experienced by the economy since Q4 of 2021.

Summer spending by consumers (Yay for Barbenheimer, the Eras and Renaissance tours, and STELLA the Dog) was a key factor in the surprisingly high growth rate. But it’s not the only economic indicator that is spewing good news. Unemployment is only at 3.8% – slightly above pre-pandemic joblessness rates.

Graph from the Wall Street Journal.

“Not only has economic output made up all the ground lost during the pandemic, but it is also above where it would have been had the pandemic never happened,” Greg Ip wrote in the Wall Street Journal earlier this week.

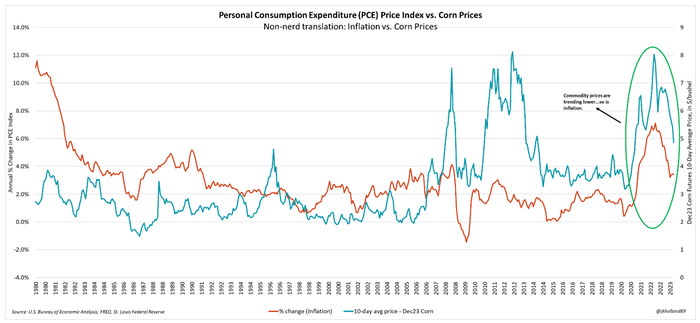

Inflation pressures remain sticky, however, which is severely eroding consumer confidence in the economy. Last week’s Personal Consumer Expenditure index, which is the Federal Reserve’s chief measurement for inflation, was reported at 3.4% for September 2023 for the third consecutive month.

There is no doubt about it – the economy is running very hot right now. Consumers are spending more as prices of some goods and services moderate, job security holds strong, and real estate equity grows.

However, consumer income and savings rates both fell over the summer months when adjusted for inflationary pressures. And though the upper-middle class (established farmers – that’s likely you) may be enjoying the recent benefits of economic growth, the average consumer’s pocketbook is increasingly squeezed by high gas prices, the re-introduction of student debt payments, record-high credit card debt, and increasing interest payments for all of those loan products.

A recession in the U.S. seems unlikely given the robust reports of current economic indicators and increasing wealth prospects for upper-middle class families. But there is no doubt that average consumers are increasingly bearing the burden of the financial challenges that continue to quietly loom over the post-pandemic economy.

In the latest round of Wall Street earnings reports, executives at food, restaurant, and snack companies have increasingly observed consumers cooking more meals from scratch and out of the pantry, consuming more leftovers, and preparing food in bulk to maximize food savings. Consumers are also being more money-conscious when eating out, opting for cheaper selections with deals, such as chicken wings and never-ending pasta bowls (SCHWING).

For farm families, there are more restaurant and grocery store discounts to be captured this fall though prices remain high. But with incomes already being stretched thin, farm families and consumers alike are showing less willingness to eat out or let food supplies go to waste. Translation: more people are eating directly from their freezers.

Food companies and ag commodities in general are fairly recession-proof bets due to their inelastic nature, though their supply chains will have to adjust to any drastic change in consumer eating habits in the near future. Humans need daily calorie intake to survive, regardless of what else is going on in the economy. While that generally favors farmers – the producers of many of the raw materials required for food processing and retail – it does not come without cost.

This dynamic creates more struggles for younger farm families, especially those who may be starting out on their own and without significant financial assistance from their more established farm elders. It also puts liquidity (cash) pressure on farm operations who have been bidding high cash rents in recent years, especially as grain and oilseed prices drift lower this fall following 2022 highs.

For farmers, interest rates staying high means that capital costs are likely to remain high through at least the 2024 operating year. More working capital (cash) may be utilized for financing instead of higher-priced credit for machinery purchases and building construction projects.

And though interest rates may be high on real estate loans, I think there is still a good argument to be made that it is a good hedge against higher land costs down the road. Land values aren’t really showing any signs of cooling, so as soon as interest rates go down, those values could continue to go up. Paying a little extra in interest now might save you on principal costs down the road.

You May Also Like

Enter a zip code to see the weather conditions for a different location.