Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

E-Corn-Omics: Markets only expect minor revisions, but remain optimistic that bearish winds for corn, soybeans could take a turn in Friday’s USDA report series.

USDA releases a series of market reports on Friday that will provide markets with the latest insights about current corn, soybean, and wheat supplies, as well as finalized (ish) usage rates for corn and soybeans for the 2022/23 (old crop) marketing year.

I’ll explain below the significance of each of these reports. But farmers should expect to see some price volatility from Friday’s report series that could impact beginning stocks for the current 2023/24 marketing year.

USDA will be publishing fresh data on June 1 – August 31 Quarterly Grain Stocks, as well as revisions for prior quarters, on Friday. It will also update production values for 2022 corn and soybean yield and production and 2023 wheat production.

As always, our team will be covering the reports in real time, offering live updates and analysis following the reports’ release. Tune into FarmFutures.com or on our social platforms (@FarmFutures) at 11 a.m. CDT on Friday for all the latest news.

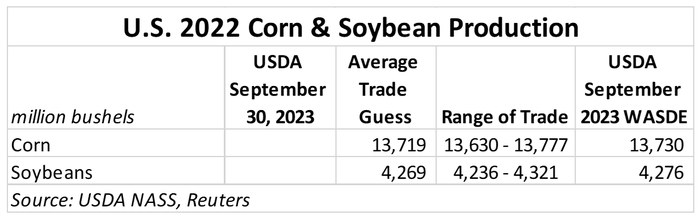

Yes, you read that right. USDA is going to do one final round of revisions to 2022 corn and soybean production in Friday’s reports. I acknowledge this may seem somewhat backwards given that harvest is already underway for the 2023 crop. But balance sheet aficionados (hi!) such as myself know that this is a necessary revision to ensure the reliability of 2022/23 usage rates and accurate 2023/24 beginning stocks volumes.

USDA-NASS’s farmer surveys, objective yield tests, satellite imagery, and squaring up with FSA and RMA acreages are all the primary methods used to evaluate crop supplies on the front end of the crop marketing year. The reliability of these estimates increases over time, with the January yield and acreage estimates widely adopted as the “final” totals.

But those supply-side estimates are only one side of the balance sheet. USDA-NASS must reconcile usage data with the supply figures to ensure accuracy and reliability. The logic is that usage rates cannot be higher than supply estimates – because you can’t use what isn’t produced.

Late revisions are never viewed favorably by market watchers and farmers, but they are essential for proper accounting of 2022/23 supplies. Collecting accurate crop supply and usage data is no small feat and is increasingly complex following five exceptional years of weather mishaps that have skewed production forecasts. So revisions to 2022/23 corn and soybean supplies should be expected and not necessarily dreaded.

Markets are expecting that the 2022/23 corn crop was likely a bit smaller than the January 2023 estimate. I’m guessing that smaller export usage figures will factor into a potential downward revision. The average pre-report trade guess for the 2022 soybean crop is also slightly smaller than current estimates.

And it’s worth noting that the market expects the 2022 corn estimate could vary between 47 million – 100 million bushels from the January 2023 finalized haul. But since the average trade guess is hovering a slight 11 million bushels lower than the current 13.73-billion-bushel estimate, it is likely we could see more price movement in the corn market on Friday’s reports if USDA’s 2022 corn figure comes in on the lower end of the spectrum.

It's a similar story for soybeans – pre-report analyst estimates for 2022 soybean production are currently 40 million – 45 million both above and below current old crop soy production estimates. It’s a tight range and since the average trade guess is only 7 million bushels lower than the current figure of 4.276 billion bushels, the only way we will see significant market movements on Friday is if USDA revises the 2022 soybean production figure by a larger amount than 40 million bushels.

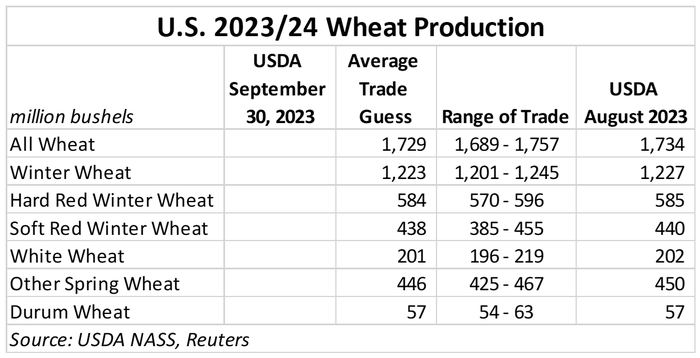

USDA has already issued several survey results for 2023 U.S. wheat production over the past several months. But with winter wheat harvest long wrapped up and spring wheat harvest winding down across the Northern Border, USDA-NASS is finally able to publish more reliable harvest estimates for the 2023 U.S. wheat crop.

I wrote an earlier column about yields and yield uncertainty that may be worth a revisit if you’re hoping for a more exciting wheat production report on Friday. But the spoiler alert is that 2023 wheat production totals are not likely to change all that much from current estimates last updated in the August 2023 WASDE report series.

I think the biggest wild card here will be the “other spring wheat” category, because harvest had not yet hit full speed when USDA last surveyed growers in late July. The pre-report market analyst guess range for spring wheat production stretches a range of 42 million bushels – a figure that is over 9% of current crop forecasts.

The average trade guess for 2023 spring wheat production assumes a slight decrease in this year’s crop. This wouldn’t be surprising – the spring wheat crop faced hot and dry conditions at heading this summer that will likely curb production forecasts.

The dark horse for U.S. wheat production? I think it could be any potential updates to soft red winter wheat production in 2023. Growing conditions were idyllic east of the Mississippi River this year, and many farmers reported record yields.

But the market is expecting USDA to slightly pare back 2023 soft red winter wheat production, which wouldn’t be a bad thing for prices as they continue to compete against Russian export volumes and earlier expectations of a bumper soft red winter wheat crop harvested this year.

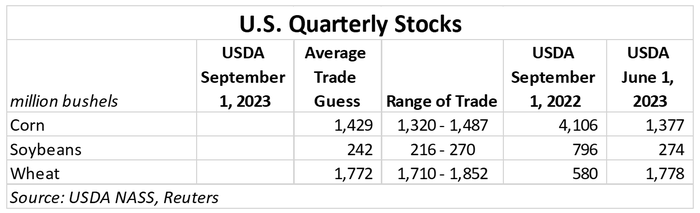

For wheat, market watchers will be deriving demand signals produced by the Quarterly Grain Stocks report. Some redneck math and accounting is required to back into usage calculations from the stocks data provided by USDA on Friday, but based on the average trade guess for June 2023 – August 2023 U.S. wheat usage it is likely we will see small Q1 wheat usage rates here in the U.S.

This is not quite a bullish surprise, though. Even before this report, we knew that three consecutive years of wheat production shortfalls would inevitably tighten wheat usage – because you can’t use what you didn’t grow.

If the average trade guess is realized, it will be the smallest Q1 wheat stocks reading since 2007/08. It seems likely that USDA will make minor cuts to 2023 U.S. wheat production in Friday’s reports as well – and this will be critical to offset any market jitters about declining usage in an era when Russian wheat exports are flooding the global market and domestic usage struggles to keep wheat prices competitive against corn and soybeans as peak winter wheat planting season ramps up.

But the hot-ticket items I will be watching in Friday’s Quarterly Grain Stocks report will be on the corn and soybean balance sheets. The average pre-report trade guess for September 1 corn stocks stands at 1.429 billion bushels. Put another way, this value represents the 2022/23 ending stocks value for U.S. corn.

That estimated value is about 13 million bushels lower than current USDA projections for 2022/23 U.S. corn ending stocks, which means that markets are hoping for a bullish report as stocks tighten and usage rises above previous expectations for the marketing year.

And it’s not like 2022/23 was a banner year for U.S. corn consumption, either. Because of the smaller crop harvested in 2022, export volumes were limited and cattle usage – historically the largest consumer of U.S. corn – waned as the herd shrunk amid widespread drought and expensive feed.

But if Friday’s report shows larger than expected Q4 usage from June 1, 2023 – August 31, 2023, farmers should be able to breathe a sigh of relief that the consumption prospects will help to offset growing supplies expected in the U.S. market with the harvest of the 2023 corn crop.

Similar to corn, markets are also bracing for slightly tighter 2022/23 soybean ending stocks. The average analyst guess ahead of Friday’s report release pegs September 1 soybean stocks (the ending value for 2022/23 U.S. soybean ending supplies) at 242 million bushels.

If realized, that would be a slightly higher Q4 soybean usage rate than previously expected – which is likely due in no small part to the addition of a new crush plant in Iowa earlier this spring. But it also means that in absolute terms, soybean stocks will drop to their smallest level since 2015/16 (197 million bushels).

It seems inevitable that Friday’s report will be at least slightly bullish for soybean prices (though I’m pretty sure NASS’s Lance Honig makes a sport of proving me wrong!). But as farmers begin to look towards 2024 acreage decisions, it’s worth noting that corn acres will continue to try to keep up with soybeans, even if Friday’s reports aren’t as bullish for corn as soybeans.

The hope among farmers is that USDA’s reports on Friday will trigger enough price movement to revive corn and soybean markets from current harvest pressure, cementing a harvest-time price low. And while the trade is certainly gunning for that outcome, we can never predict USDA’s outcomes with significant levels of certainty leading up to report releases.

But with a large 2023 corn crop on the horizon and increasing demand challenges facing the corn market, tighter 2022/23 ending corn stocks would be a welcome reprieve from recent bearish price action. December 2023 corn futures prices have already fallen 22% since USDA’s last Quarterly Grain Stocks report in late June.

November 2023 soybean prices have only fallen 11% during that time, which suggests that the tight supply situation for soybeans is helping to insulate prices from larger losses. We will need to see strong Q4 usage data to support that estimation from Friday’s USDA reports and to maintain some price stability for the soybean complex as harvest ramps up.

You May Also Like

Enter a zip code to see the weather conditions for a different location.