Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

E-Corn-Omics: Corn, soybean production will change next month when USDA adjusts acreage. Plus, other key August WASDE insights.

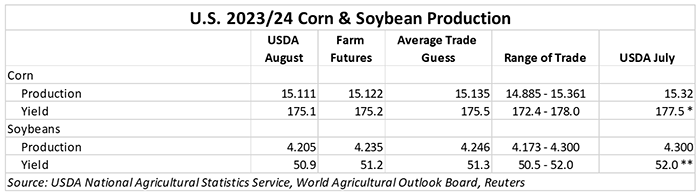

The August USDA report series is one of the most anticipated report days of the marketing year for farmers and market players alike. It marks the first time in the growing season that USDA surveys farmers for their estimates for corn and soybean yields – prior to that point, estimates derived from economic models are used.

It is still early in the growing season as far as yield estimates go, which means there is still a high chance that USDA will shift yield estimates in the coming months. However, USDA’s yield estimates on Friday came in quite close to our team’s surveyed yields from our August 2023 survey, which was a pleasant surprise for this analyst!

But beyond my emotional investment in Friday’s reports, there really weren’t a lot of surprises in USDA’s findings. Here’s my quick two cents on the August 2023 Crop Production and World Agricultural Supply and Demand Estimates reports.

Both of USDA’s corn and soybean yield estimate figures came in slightly below the pre-report average analyst guess on Friday. I wasn’t really surprised by this – it was a timing issue that market players commonly have to deal with in the August USDA report series.

Based on the timing of NASS’s July/August surveys, I wasn’t surprised that farmer responses indicated a lower yield number. Some of those responses were reported before we saw cooler temperatures and more rain at the beginning of the month, as the NASS farmer survey ended on August 1.

But I think that opens the door to future upward yield revisions if these favorable weather conditions continue – and it looks like they will for at least another couple weeks. That means that we could see higher yield estimates in September, October WASDE and Crop Production reports, which would likely increase supplies and be bearish for prices.

The 2023 corn crop is expected to be a massive 10% bigger than last year’s harvest, despite Friday’s yield downgrades. Meanwhile, smaller acreages will put this year’s soybean haul 2% smaller than last year’s.

I think as long as we see demand growth – whether that be from domestic biofuel markets or international export purchases – prices will remain moderately high, though this bigger supply environment will still keep prices off of the 2022 highs we saw in the aftermath of the Black Sea conflict.

There is still plenty of time left in this growing season for yields to improve – or dramatically fold, as we’ve seen in previous years (i.e., the August 2020 Iowa derecho). Plus, NASS has yet to revise corn and soybean acreages to account for Risk Management Agency (RMA) acreage data. Some Farm Service Agency (FSA) data was evaluated for yields in this month’s report, but an acreage update will shift production forecasts in September.

It is still early in the yield-guessing game, so we don’t get to be surprised next month (or the following month) when USDA inevitably changes production estimates.

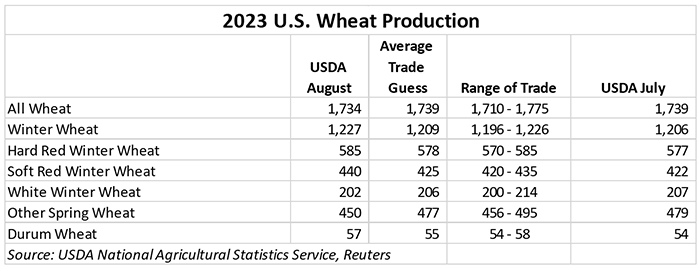

NASS did use finalized FSA and RMA data to revise wheat acreage. However, 200,000 additional planted and harvested wheat acres could not overcome a 0.3 bpa yield cut for 2023 U.S. wheat production, which left the 2023 wheat harvest 5 million bushels smaller than previous estimates at 1.734 billion bushels.

That figure remains to be an 84-million-bushel increase over the 2022 U.S. wheat crop. Some old crop balance sheet revisions paired with lower new crop export expectations helped push 2023/24 U.S. wheat ending stocks higher in Friday’s report, which was a bearish price signal for the wheat market, even though a smaller crop was projected for 2023.

The export slash and smaller spring wheat crop was the big surprise in my mind following the report’s release. I think this emphasizes the need for domestic wheat usage in the coming months to maintain price stability, otherwise I think we will see 2024 winter wheat acres contract. Remember – we aren’t that far away from winter wheat planting, so these market dynamics will be important to watch over the coming months.

And could we please just go one growing cycle with somewhat normal conditions for this wheat crop?!

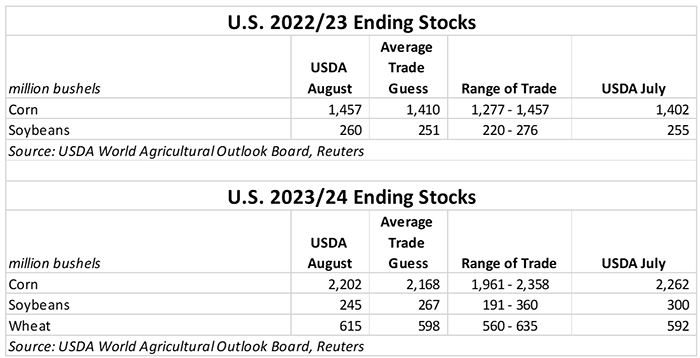

Old crop corn and wheat usage estimates were cut, which added in some additional demand liquidity to 2023/24 demand pipelines for both crops. Translation: lackluster demand for 2022 corn and wheat supplies helped add on to 2023 beginning supplies, which was slightly bearish for 2023 corn and wheat futures prices.

But soybean supplies will continue to remain tight, due in large part to the smaller yields and acreages expected to be harvested this fall compared to where we thought we started this spring.

Because smaller corn yields take such a big bite out of supply availability, corn usage estimates for food, feed, and exports were all metered lower for the upcoming 2023/24 marketing year. Wheat food use estimates were also slightly trimmed.

But for all three primary crops, USDA implemented sizeable cuts to 2023/24 export forecasts. Corn exports (50M bu.) saw the biggest cut, with soybeans and wheat each enduring a 25-million-bushel reduction individually.

It’s no secret that expanding corn and soybean production in Brazil (and less storage capacity), as well as wheat production in Russia and the European Union, are out-competing U.S. supplies and shifting the window of export opportunities in unexpected ways for U.S. producers.

This means that farmers will be more reliant on domestic markets to generate pricing opportunities over the coming months. Wheat has seen somewhat of a revivial in human consumption in recent years, though lower prices could entice more feed demand as well. Soybeans are going to be in good shape as more renewable diesel plants come online over the next couple years (though we could afford to bring on more capacity).

But corn will be the biggest wild card. Despite flatlined ethanol blending requirements outlined by the EPA for the next three years earlier this summer, ethanol continues to be a bright spot for corn usage this summer, so I was relieved that USDA left 2023 ethanol estimates untouched in Friday’s report.

We will need to see refreshed pastures across the Heartland and hay supply rebuilding signs in the cattle market to ensure that more cows will be eating more corn going forward. In the absence of the export market, I think U.S. corn producers will become increasingly dependent upon cattle consumption in the 2023/24 marketing year for pricing opportunities.

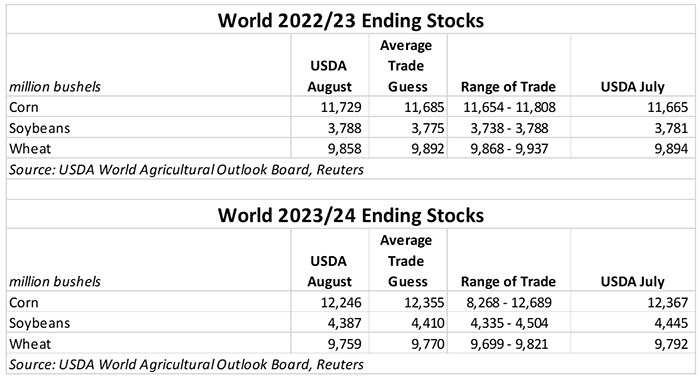

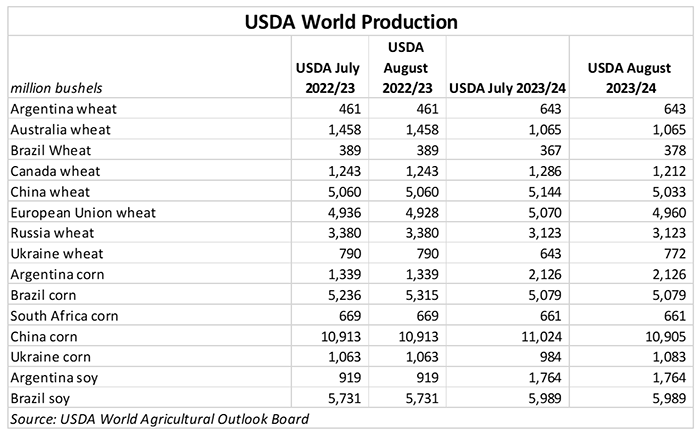

World stocks estimates were largely impacted on Friday by Northern Hemisphere crop projections and revisions. Especially for wheat – even with upward harvest revisions for Ukraine, lower crops due to turbulent growing seasons in the E.U., China, and Canada took a larger than expected bite out of global wheat stocks.

This should keep somewhat of a price floor under global wheat prices going forward, though U.S. prices will still be pressured by a stronger dollar and logistical constraints (relative to countries in the Eastern Hemisphere). I think the biggest factor that will trigger wheat price movement going forward thence becomes Russia’s wheat crop and the pace at which it can export it under current market (whether that be black market or otherwise) conditions.

The smaller U.S. corn crop compounded with crop damage in China, tightening global stocks. Ukraine’s corn production will be slightly better than expected this season, but will it even matter if Ukraine can’t get any grain shipped out of the Black Sea?

Meanwhile, the tightened global soy balance sheet was a direct reflection of the smaller 2023 U.S. soybean crop. Brazil will inevitably plant more soybean acres this fall, but if El Niño weather conditions favor production (spoiler alert – it’s highly likely they will), global stocks could surge upwards by next spring.

Read more about:

WASDEYou May Also Like

Enter a zip code to see the weather conditions for a different location.