Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Markets will be watching for Argentine corn, soybean production cuts and potentially larger global wheat supplies.

The February 2023 World Agricultural Supply and Demand Estimates report from USDA is not likely to be near the market mover as is the January report series. That’s because no supply adjustments will be made to U.S. corn, soybeans and wheat, which helps reduce some of the market volatility that has come to be associated with USDA reports.

Here is what I will be watching the markets for leading up to tomorrow’s reports.

As always, our team at Farm Futures will be covering the reports live and providing ongoing analysis. USDA publishes the reports at 11 a.m. CST. Check out our website, FarmFutures.com, as well as our social platforms, @FarmFutures, for the latest insights!

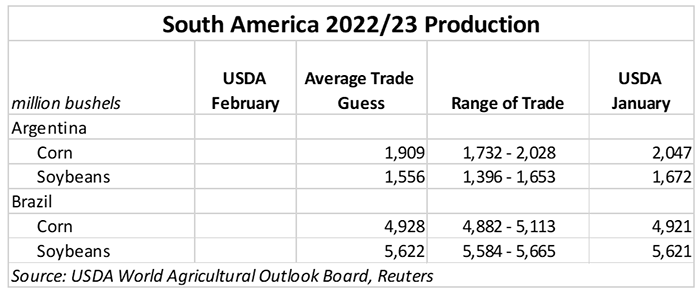

South American corn and soybean production will be the big-ticket item for tomorrow’s WASDE report. The biggest cuts are expected to be made to Argentina’s corn and soybean crops, and while there is potential for USDA to increase the size of Brazil’s corn crop, traders don’t expect any revisions will be made tomorrow.

Argentina’s drought is beginning to show signs of ending as La Niña finally begins to relent after three long years. Southern Brazil continues to battle dry conditions, where some crop risks remain. But heavy rainfall in Mato Grosso over recent weeks is expected to give way to drier weather over the next 10 days that should aid soybean harvest and second crop corn planting.

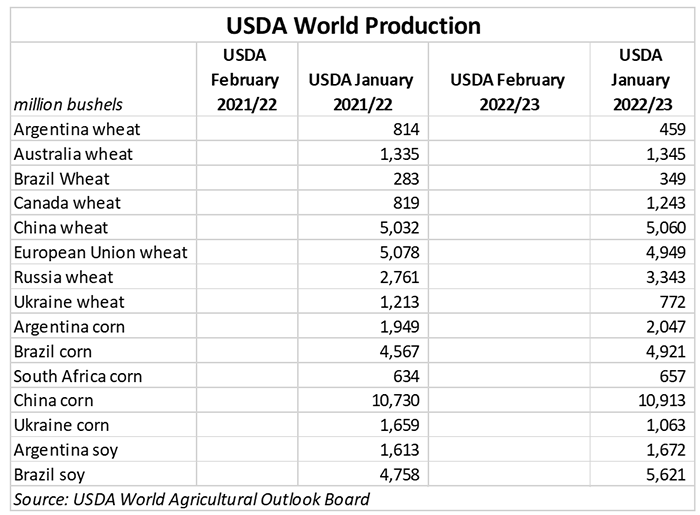

USDA attaché reports published in recent weeks found that Brazil’s corn production forecasts for the 2022/23 marketing year were increased by 0.4% from USDA’s current forecasts to 4.941 billion bushels. Market analysts do not think USDA will make significant changes to Brazilian corn and soybean production in tomorrow’s reports, so if an upward revision is made to corn figures, bearish price action could be in order.

Another USDA attaché in Argentina is calling for even further cuts to Argentina’s soybean crop. The attaché expects the 2022/23 Argentine soybean crop will only reach 1.323 billion bushels – a staggering 349 million bushels fewer than USDA’s current estimates, which already saw a big 147-million-bushel cut in the January 2023 WASDE.

"Dry weather and high temperatures in the last months of 2022 have damaged the marketing year 2022/23 Argentine soybean crop, particularly affecting first crop soybeans within a 125-kilometer radius of Rosario, Santa Fe Province. Recent rains will buy time for second crop soybeans, but better-than-average weather through February is needed for a substantial recovery,” the attaché report stated.

The market is also expecting big cuts to Argentine corn production for the 2022/23 growing season. USDA revised Argentina’s corn harvest 118 million bushels lower in January 2023. Pre-report trade guesses peg Wednesday’s downward revision at 138 million bushels.

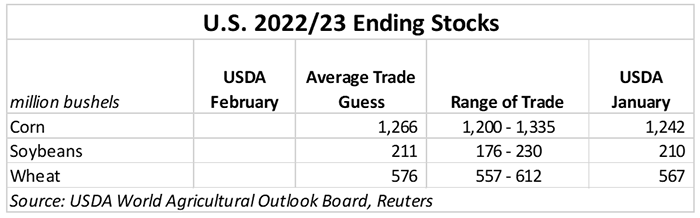

Pre-report trade estimates are not expecting much movement for soybean and wheat stocks in the February WASDE. So, if USDA makes any demand adjustments to U.S. soybean or wheat usage on Wednesday, there could be some unexpected price volatility in both of those price complexes.

But changes are likely unavoidable for corn usage metrics. On average, analysts expect 2022/23 U.S. corn ending stocks will grow by 24 million bushels from last month’s estimate to 1.266 billion bushels. But where will USDA make these cuts?

USDA made sweeping cuts to 2022/23 U.S. corn usage in the January 2023 WASDE, slashing a total of 185 million bushels from the corn demand pipeline this marketing year (150M of those bushels came from export reductions).

Last week, USDA-NASS announced the size of the U.S. cattle herd had shrunk to a 61-year low following persistent drought conditions in the Plains and soaring feed prices. I think the chances are highest that USDA will make cuts to the feed and usage category, though slow corn consumption for ethanol rates in late December 2022 could also call for a slight downturn for corn usage for ethanol metrics.

Corn exports remain lackluster, but shipping paces are little changed in the past month which will likely result in no changes being made to corn export figures tomorrow. While current marketing year outstanding export sales are still 49% lower than year ago values, that figure has risen by 12% over the past month. A year prior at that time, outstanding export sales shrunk by 1%.

There are other market dynamics that will also impact South American crop production in the coming months – Brazil’s currency, the real, is also expected to continue weakening over the next 9 months, according to a recent Reuters foreign exchange poll. Brazilian President Luiz Inacio Lula da Silva has spent his early days in office railing against the Brazilian central bank for keeping prohibitively high interest rates in place.

The high rates are a hindrance to da Silva’s agenda, which is focused on social issues. The real has risen 1% since January 1, 2023 but is expected to fall 1.7% in the next 12 months to 5.24 real/U.S. dollar. As of yesterday, the real was trading at 5.15 real/U.S. dollar.

The weaker real will make Brazilian soybean and corn exports a more affordable option on the global market, especially when priced against more costly U.S. supplies. So not only will South American production values be closely watched in tomorrow’s WASDE, but Brazil and Argentina’s corn and soybean export values will likely generate additional market movement.

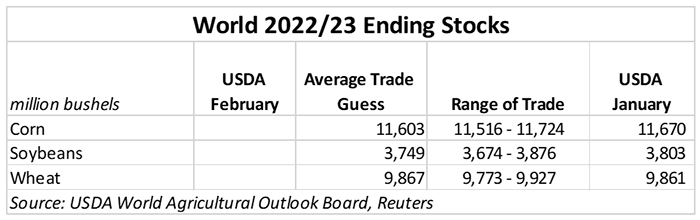

The results of any downward Argentine corn and soybean supply changes are likely to be the key drivers of tightening global corn and soybean stocks expected in the pre-report analyst estimates ahead of tomorrow’s WASDE report.

An annual improvement in Canadian wheat production according to USDA’s attaché post in Ottawa will likely result in larger global wheat ending stock volumes in tomorrow’s report. The post calculates a 50%-plus increase in annual Canadian wheat production thanks to larger planted area and improved soil moisture, bringing the 2022/23 harvest to 1.242 billion bushels.

“Wheat exports are forecast to increase year-over-year on larger domestic supplies and strong demand from China, Japan, Indonesia, and South America,” the attaché report stated. The larger Canadian wheat supply will likely grow global wheat supplies and be a bearish factor on wheat prices.

That’s good news for Canadian cattle producers, who were heavily reliant on U.S. feed imports last winter. However, that is yet another bearish factor weighing on U.S. corn and wheat export markets.

USDA’s attaché in Canberra, Australia is calling for USDA to increase the Aussie’s 2022/23 wheat harvest by 1% to 1.359 billion bushels. It marks the third consecutive year of record-breaking wheat crops for Australia and exports are expected to set new records as well amid ongoing turmoil in the Black Sea.

That supply increase will likely be bearish for global wheat prices, especially as markets are already expecting global ending wheat stocks to increase slightly in tomorrow’s report.

The USDA attaché in Beijing cited competitive Brazilian corn prices as an incentive to keep China buying more Brazilian corn in the coming months.

“Feed mills [in China] have resumed mixing more corn in feed rations as higher prices for wheat and sorghum reduce demand for corn alternatives. At the same time, Brazilian corn is now available and priced competitively with domestic corn... With the arrival of the first vessel of Brazilian corn in early January 2023, China will likely turn to Brazil for a substantial amount of its corn imports."

If USDA decides to change any of China’s corn or soybean import volumes tomorrow, I expect that will provide little benefit to U.S. corn prices, as Chinese buyers increasingly spurn U.S. corn supplies in favor of cheaper Brazilian alternatives.

The USDA attaché in Mexico City expects that Mexico will need to increase its current corn imports during the 2022/23 marketing year after revised planting data resulted in a smaller production value. The post is now calling for USDA to increase Mexico’s 2022/23 corn imports to 681 million bushels, up 4 million bushels from the current forecasts, but still lower than last year’s shipments that totaled 692 million bushels.

That’s not a significant increase, but it is a lone spot for bullish price opportunity for U.S. corn exports.

Read more about:

WASDEYou May Also Like

Enter a zip code to see the weather conditions for a different location.