Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

There is likely no short-supply-induced rally in the works for old crop prices.

USDA’s supply/demand adjustments to their old crop world cotton balance sheet showed a small net decrease in world-ending stocks. There really weren’t that many changes compared to the previous month.

On the supply side, there was barely any change in beginning stocks. World production was 1.03 million bales fewer than the January forecast, mostly in India (-1.0 million), West Africa (-610,000), which month-over-month increases in China (+500,000) and Pakistan (+200,000). World imports were 1.19 million bales fewer, month over month, from reductions in Pakistan (-500,000), Indonesia (-300,000), Bangladesh (-100,000), Vietnam (-100,000), and Mexico (-50,000).

On the demand side, world domestic use was 190,000 bales fewer, month over month, due to decreases in Pakistan (-200,000), Indonesia (-200,000), the U.S. (-100,000) and Vietnam (-100,000) that outweighed a half million bale increase in China. World exports were 1.28 million bales fewer compared to January, with the major adjustments coming in India (-600,000), West Africa (-460,000), Brazil (-300,000), and the EU (-10,000), all of which outweighed a 200,000-bale increase in Australia.

The bottom line of all the world adjustments was neutral to modestly bullish. We’ll have to see what the earthquake damage in Turkey does to their cotton production and milling sectors, both of which are in the affected region.

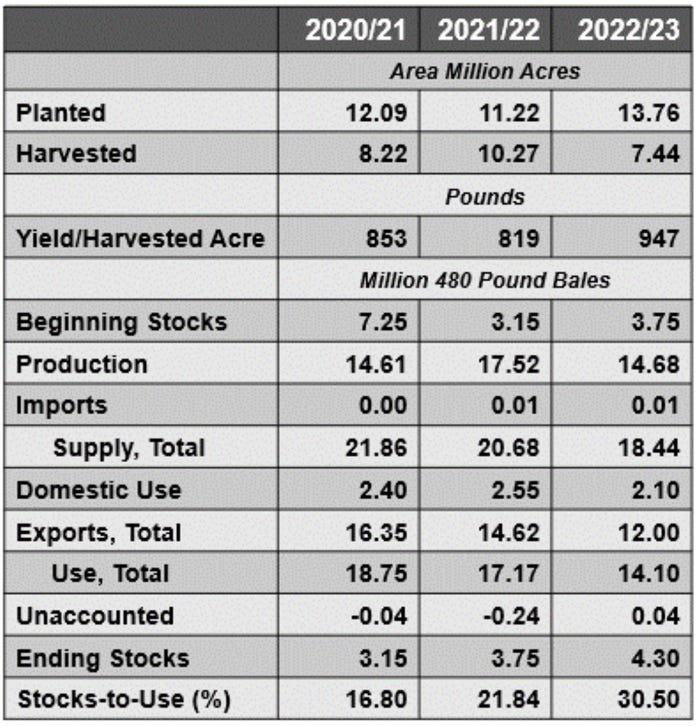

USDA’s February WASDE mostly kicked the can down the road for the U.S. cotton old crop balance sheet. USDA cut domestic cotton consumption by 100,000 bales, which was then added to raise ending stocks to 4.3 million bales (see U.S. cotton balance sheet below).The supply side of the U.S. balance sheet was unchanged. The earlier discrepancy between bales produced versus bales ginned appears to be resolving by higher-than-expected (by me) ginnings. The moral to that story is that there is likely no short-supply-induced rally in the works for old crop prices.

For additional thoughts on these and other cotton marketing topics, please visit my weekly on-line newsletter at http://agrilife.org/cottonmarketing/

February 8, 2023 World Agricultural Supply and Demand Estimates, USDA/OCE.

You May Also Like

Enter a zip code to see the weather conditions for a different location.