Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

February 1, 2013

Don’t let that frighten you. And don’t jump off a cliff. I throw that number out there more for conversation purposes than an outright prediction. On the other hand, if history repeats itself, that is likely the downside target for soybeans. This is a potentially very bearish situation soybean producers could be facing in the next several months.

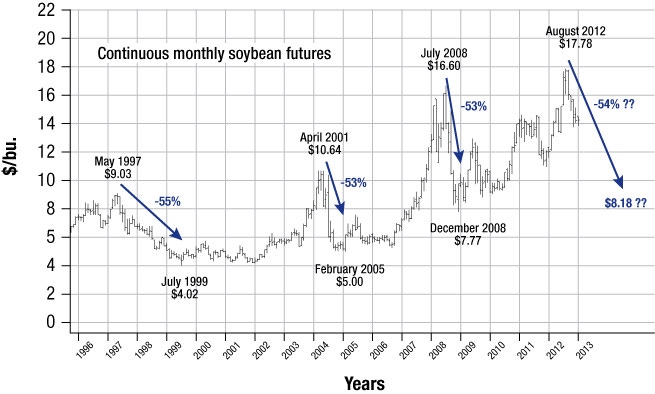

The chart above displays a very interesting potential scenario. After peaking in May 1997 at $9.03, the market declined to $4.02 by July 1999, a 55% drop in prices. In April 2004 the market peaked at $10.64 and dropped to $4.99 – a decline of 53%.

July 2008 witnessed a top price of $16.60 followed by a drop into December 2008 at $7.77, a 54% decline.

It is frightening that the percent declines have been almost identical in the past three bear markets. If this particular market declines 54% from the August peak at $17.78, the downside target becomes $8.18.

The important question to ask now is what are the probabilities and possibilities of this happening. I like to separate market information into three categories; possibilities, probabilities and facts.

The facts that we know in this market include:

1. The trend is down.

2. Short crops peak early and have a long tail. This is a short crop.

3. Never store a short crop; always store a record crop.

4. It’s not the news that you know is important; it is the news you do not know that is important.

5. On the positive side, the soybean market is extremely oversold technically.

6. Chinese demand continues very strong. While we do not expect it to grow, we don’t look for any major setbacks either.

Now let’s take a look at some possibilities:

1. Yield increases start to kick in. Genetic improvements in soybean yields have not matched those of corn. Could this be the year?

2. Increased acreage? We don’t think so, but there is certainly a reasonable possibility that northern Illinois and northern Iowa will see some increased acreage due to yield drag of continuous corn. We believe that much of that increase, however, will be offset by decreases in soybean acreage in the south.

3. A big Brazilian and a strong Argentine crop appear to be on the way. That in itself could be all the fuel that is needed to keep the major bear market in soybeans going.

4. A slowdown in Chinese purchases? As weak as the world economy is, it’s a possibility but we would not throw it in to the category of a probability.

The bull side?

From price levels above $13.50, the only “possibility” would be major production problems in the U.S. this spring and summer. That is a long shot from this price level, considering the cut in demand over the last nine months.

So what does it all mean? To me it means this is not a year to be storing soybeans. It is a year to be a very aggressive forward seller. Prices are still very profitable, and the risk on the downside is greater than the potential on the upside. Lock in profits in a market like this when you have a chance.

You May Also Like

Enter a zip code to see the weather conditions for a different location.