Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

What does an accountant who’s married to a farmer do to prepare for lender meetings? Here’s a look.

Cheryl Martin has two items at the top of her farm finance wish list: an accrual income statement and a balance sheet.

Why? “A tax return and a cash basis statement don’t let you know what you actually made,” says Martin, a lifelong accountant and partner at Kerber, Eck and Braeckel, in Springfield, Ill. She farms with her husband, Tom, near Mount Pulaski.

Plus, their banker really likes it.

Accrual accounting may be a topic that often appears in farm magazines, but only because lenders appreciate the clear picture it provides, and ag economists know it’s the only way to gauge profitability. “A farmer needs to see their accrual basis income statement, and they need to know where they ended the year,” Martin says, adding it’s even better if you can look at it on a farm-by-farm basis.

Dwight Raab at Illinois Farm Business Farm Management agrees, adding that the only thing better than an accrual income statement and a balance sheet is a series of those two documents from several years past.

What does an accrual income statement do? It measures net revenue income that results from the fruits of your management skills and the economic environment in which your farm operates.

Martin recommends the following when you put together an accrual basis income statement:

• Accrue grain. “In recording your grain sales (receivable), for the bushels sold, record it at what you have sold it for. For those not sold, estimate based on current prices — but let your lender know how you arrived at the grain sales number,” she recommends.

• Accrue income taxes to the correct year.

• Make sure all payables to chemical or fertilizer dealers are listed.

• Consider rents payables; some are not paid until the January after the crop.

• Know interest costs and accrue them to the correct year.

• If you’ve purchased equipment with someone, make sure the asset and debt are accounted for.

• Record revenue from grain sold with the year it’s produced. For example, say you haven’t taken any income on the 2018 crop, but you expect to receive $1 million after the first of the year, based on bushels sold. Record that revenue for the 2018 crop, not 2019. “Only reflect on your statement what your income will be on the 2018 crop,” Martin says.

How do you to accrue the potential trade war soybean payment? “That payment relates to 2018 and should be recorded in 2018. You may not receive it until 2019, but I believe the amount you will receive is now known,” she adds.

Martin says she doesn’t update their spreadsheet very often — think annually for the accrual income statement. “I only do the accrual basis annually because I know lenders want to see it,” she explains. “During the year, you have to make too many assumptions for it to be meaningful.”

Balanced and more

On your balance sheet, make sure you account for every asset — even those that seem minor. Martin points to cooperative stock, retirement accounts and ethanol plant stock as prime examples of assets that are often forgotten. A good balance sheet will also separately account for joint assets, his assets and her assets.

Martin will also run a liquidity ratio and a debt-to-asset ratio so she and her husband will know exactly where the farm is at by the end of the year. And, she keeps a separate tab on the balance sheet that lists all debt, including current maturities of long-term debt.

The Martins spend a lot of time talking about finances. Whenever they read a magazine or newspaper story that quotes benchmarks for, say, debt-to-asset, they run their own numbers to compare where they’re at. “Sometimes we realize we figure it differently or we don’t put importance on the same figures they do,” Martin says.

“I don’t get involved in whether to buy a piece of equipment, but I get involved in when and how to finance it,” she says. “In that way, we’re a team. We think about it and challenge each other, and analyze where we’re at with working capital.”

Working capital (current assets minus current liabilities) is paramount to everything, Martin says, putting on her loan review hat. “That tells me whether the farmer can repay debts.”

She says their Farm Credit lender measures working capital divided by gross receipts, which they want to see at about 15% — and they’d really like it above 30%. They also read in a recent farm publication that working capital per acre should be above $200 per acre. Below $100 is a red flag.

“I went and calculated ours because I’ve never done it per acre!” Martin says.

Gas in the tank

Illinois FBFM’s Raab looks at working capital as gas in the tank. Working capital is a flat dollar value, which is hard to assess or measure. If you divide it by acres, you get working capital per acre. If you divide working capital by total expenses, you get a percentage.

“What percentage of my total expenses are in working capital?” he asks. “That’s my gas gauge.”

If working capital as a percentage of total expenses is 100%, you have enough in working capital to finance next year’s crop. If you have no working capital, you have to borrow everything. A farm needs an “adequate” amount of working capital to weather the ups and downs of financial cycles. What’s adequate? It depends on a lot of factors, including the size of the operation and the risk associated with it.

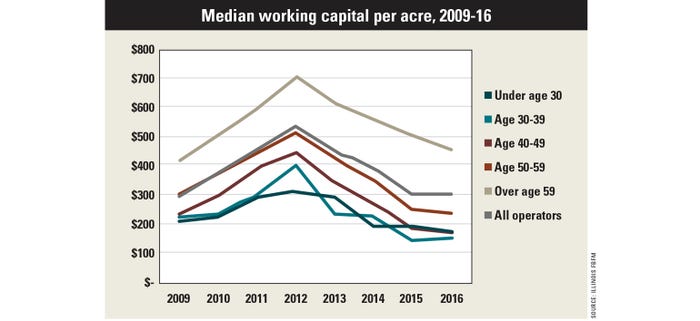

Over time, Raab has found correlation between age of a farmer and working capital (see chart below). The same is true of debt-to-asset ratio, which tends to be greater for younger farm operators, and lesser for older farm operators who’ve had a lifetime to pay down debt acquired when they were younger.

Raab says debt-to-asset ratios are like an aircraft carrier: slow to turn. You won’t fix a ratio overnight, but what you do in the next three to five years will change it. In short, your debts divided by your assets shows what you owe your lender. Or in other words, it shows how much of your business your lender owns and how much you own.

“Lenders don’t like to be in a situation where they own more than you do,” he adds.

Martin, an accountant by profession, acknowledges that accounting for farmers is complicated. And it can be hard to understand. But it’s still important.

“There is no substitute for a good set of financial records that can be used to make decisions,” she says, adding that she and her husband spend more time on numbers now than ever before.

In the end, though, her advice is the same: Make sure you have an accrual-based income statement.

Want to know how to figure some of the ratios lenders may ask for? Here’s a look, courtesy of Illinois FBFM.

Working Capital to Value of Farm Production

Computation: working capital (current assets minus current liabilities) divided by value of farm production (VFP)

Interpretation: Working capital is a measure of the amount of funds available to purchase inputs after the sale of current assets and the payment of all current liabilities. Working capital compared to VFP relates the amount of working capital to the size of the operation. The higher the ratio, the more liquidity the farm operation has to meet current obligations.

Debt to Asset

Computation: total debt divided by total assets (fair market value)

Interpretation: This ratio is another way of expressing the risk exposure of the farm business (debt divided by (debt plus equity)).

Interest Expense Ratio

Computation: total farm interest expense divided by VFP

Interpretation: The relationship of interest expense to VFP is often used as a measure of the financial risk of the farm operation.

Current Ratio

Computation: current assets divided by current liabilities

Interpretation: This ratio is a measure of the farmer’s ability to meet short-run obligations without disrupting the ongoing business. The higher the ratio, the more “cushion” the farmer has in meeting his or her current obligations. This ratio may be limited by the quality of the assets and/or the ability to quickly convert the specific current assets into cash.

Find more ratio explanations online: bit.ly/farmratio.

You May Also Like

Enter a zip code to see the weather conditions for a different location.