Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Will stocks tally help grain storage bets pay off?

A wide range of 2023 acreage estimates should have all eyes focused on March 31 Prospective Plantings this coming Friday. But a less visible USDA report that drops simultaneously could return attention back to old crop inventories as farmers try to make their grain storage strategies pay off.

Bullish numbers are always welcomed by growers, but a friendly quarterly Grain Stocks print would be especially welcomed after sixth months of sluggish markets. Soybeans locked up in on-farm storage at harvest may have netted a few pennies after costs for interest and handling. But corn put in the bin, on average, is in the red.

Without a surprise in the stocks data, old crop futures likely will live or die with USDA’s survey of growers’ planting plans for spring. But March 1 inventories, though tricky to interpret, have at times been the main story from these big data dumps.

While acreage deals with new crop supply, Grain Stocks are a measure old crop demand -- in this case, how much was used during the second quarter of the marketing year from December through February. The difference, or “disappearance” between March 1 and December 1 stocks, presumably was consumed by end users.

A lot of those corn and soybeans went to processors turning them into biofuels, seed, and other products. Exporters also took their share, moving the grain around the world.

This demand is relatively easy to track. The Census Bureau reports monthly exports as well as domestic consumption of corn for ethanol production and soybean crush. December and January Census numbers are in, and the February totals can be estimated from weekly reports on ethanol production and exports, as well as monthly soybean crush already put out by the National Oilseed Processors Association. Usage for seed, food and other industrial purposes doesn’t vary that much as a rule.

But USDA also measures another, murkier category called residual usage. This is the amount that “disappeared” during the quarter but can’t be accounted for otherwise.

The government has no way of directly measuring how much corn is fed to livestock, so most of this unexplained demand is assumed to have walked off the farm.

USDA surveys growers and commercial firms to make its stocks estimates. So, some of this residual usage is also due to statistical noise contained in any type of survey data. But on occasion the discrepancies are large enough to move the market.

For corn, there’s always the possibility that livestock feeding was more than expected. That may have been the case during the fall. Cattle feeding was profitable during the quarter, though farrow-to-finish hog operations struggled to break even. USDA’s Dec. 1 stocks indicated 46% of the year’s feeding likely took place during the September-November quarter, more than the 41% long-term average for fall consumption.

But higher-than-expected disappearance during the second quarter doesn’t seem likely, because livestock margins were mostly under pressure this winter.

Soybean residual is much smaller than corn and some quarters is even negative as the government corrects accounting errors. But September-November soybean residual usage of 186 million bushels was also more than historically projected for the quarter.

Additional discrepancies in the second quarter could be a hint of something more than just normal statistical error.

I estimate March 1 corn stocks at 7.41 billion bushels, with soybeans at 1.666 billion. If March 1 stocks are significantly less on March 31, it could be a clue that 2022 crops were smaller than reported in January, when USDA made its final monthly estimate.

Remember, USDA’s January corn production estimate fell by 200 million bushels, with soybeans down 70 million. Some acres were also unharvested, adding to the uncertainty.

USDA puts out “final” old crop production estimates at the end September, so it will be another six months before the true story is known. In the meantime, big swings in 2023 acreage could make remaining old crop either more – or less -- valuable.

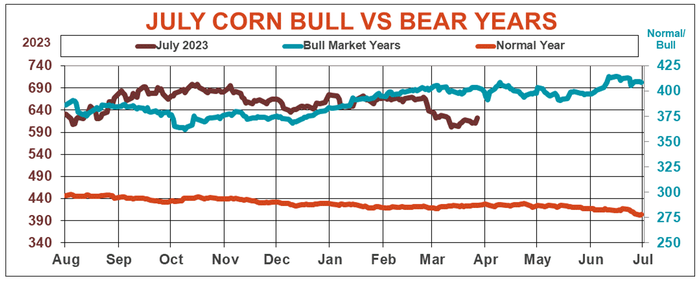

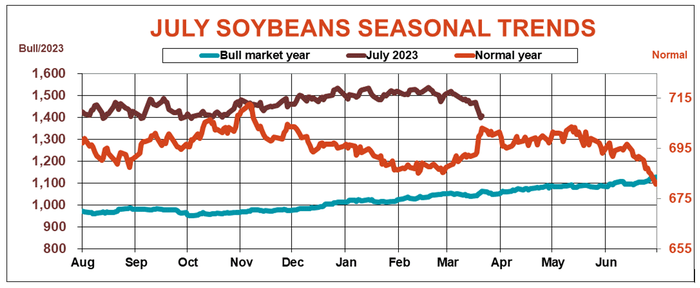

Both corn and soybeans need help according to seasonal charts. July corn futures show a persistent pattern of lower lows and lower highs. July soybeans followed a more bullish trend until failing to make new highs in March while faltering to test harvest lows. This puts both crops on the tracks seen during normal years. Modest gains through April on average are possible if this continues, but occur barely half of the time for soybeans and 40% of the time for corn.

Flipping the script won’t be easy.

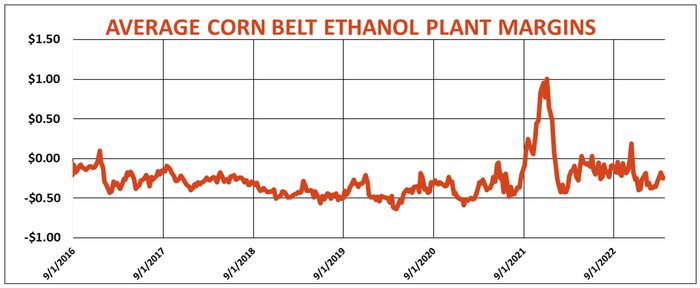

Biofuel margins accumulated losses over the winter after a promising fall, and the plunge in energy markets in March due to the banking crisis has deepened the red ink.

USDA currently forecasts corn use for ethanol down 1.3% from 2022 crop levels Estimated consumption to date is down 5% and the latest forecast from the U.S. Energy Information Administration is off 2.5%, though that agency also predicts a slight year-on-year increase in blending for gasoline.

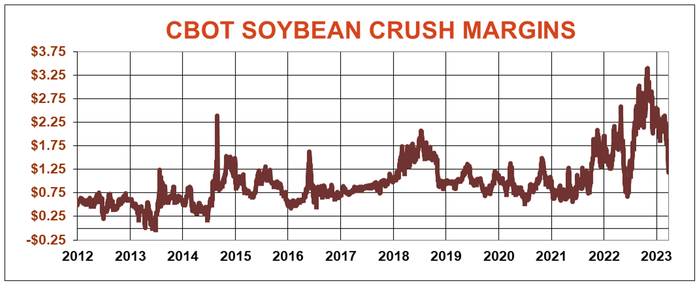

Less data is available for biodiesel, but crushers so far don’t appear to be ramping up for what many hope is a boom in the next year. Usage to make soy biodiesel through December was up 5.7% from the prior year, but that was a drop in the bucket after a huge falloff in soybean oil exports.

Exports traditionally are the swing factor in demand, helped by a booming global economy or production problems elsewhere among major producing countries. Don’t look for bullish demand surprises from consumers with thinner wallets. Inflation and the latest banking crisis, which is still unfolding, appear to be eroding spending power abroad.

Chinese soybean demand is improving following strict COVID lockdowns, but imports are still likely to fall below higher levels in seen in 2019-20 and 2020-21 after the end of the trade war. Total U.S. soybean exports are expected to be down year-on-year, though they may be a little better than USDA forecasts depending on how much a big crop in Brazil offsets losses from severe drought in Argentina.

China could also be a factor making the corn outlook might more interesting.

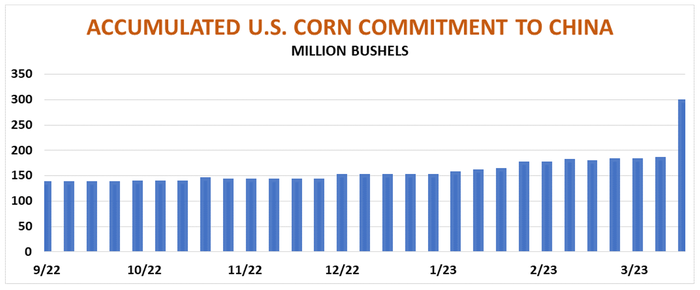

Though total U.S. corn sales and shipments to China through last week are down 44% year-on-year, the world’s largest soybean importer also bought U.S. corn aggressively earlier this month as nearby futures slipped to the lowest level since August. March sales appear to total around 150 million bushels so far, helping the total to all destinations reach a marketing year high last week.

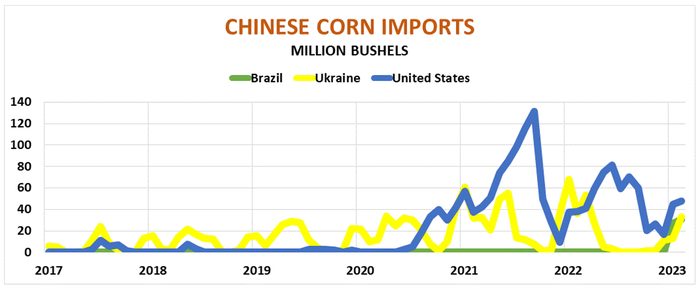

As good as recent corn sales were, it’s far from clear they’ll persist or just be a drop in the bucket. U.S. sales to China took off at the end of the 2020-21 marketing year. A bad crop in Ukraine, China’s traditional supplier since a 2012 grain deal, opened the door for the U.S., which later benefited from closure of Ukraine ports following Russia’s invasion.

But this year U.S. growers have a new competitor – Brazil. China approved imports from the South American ag powerhouse last fall, slowing U.S. sales until the recent flurry.

So far, Brazil’s 2022-23 production looks good, though that outlook hinges on its big second crop “safrinha” corn, which is planted behind soybeans and won’t be harvested until summer in the northern hemisphere. Mounting tension between the U.S. and China may not be good for business, either, if trade war habits from Beijing return.

Growers do have one key market barometer to watch. The CFTC has finally begun releasing updated Commitment of Traders data outlining money flow, after problems with its reporting system.

Big speculators began liquidating a net long position in corn in the last two weeks of February, selling that intensified after the banking crisis forced these hedge funds to abandon risky bets in many markets. In all, these funds dumped $3 billion in corn futures before trimming bearish bets a little last week. Funds’ net short position is a long ways from the record set in the summer of 2020, during the height of the pandemic, if the mood really sours again.

Interest in soybeans held up longer but has wavered the last two weeks. A change in sentiment in either market could be an important turning point, but one that won’t come easy. Still, if the funds start buying in earnest, the market could finally get a welcomed leg higher.

Knorr writes from Chicago, Ill. Email him at [email protected].

The opinions of the author are not necessarily those of Farm Futures or Farm Progress.

You May Also Like

Enter a zip code to see the weather conditions for a different location.