Subscribe to receive top agriculture news

Be informed daily with these free e-newsletters

Profit potential still looks good for 2023 production.

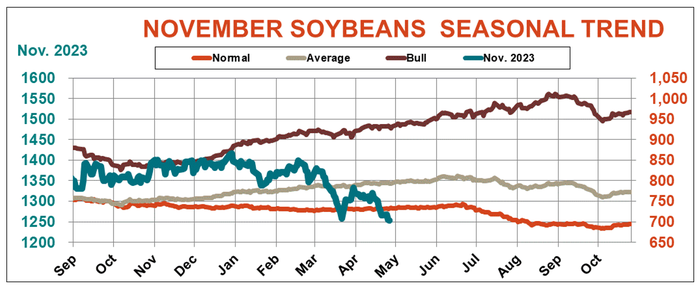

Soybeans ended April on their back foot, losing more than 75 cents of gains made on a late March bounce. Still, though November futures hover just above nine-month lows, the news isn’t all bad. The average grower has a good chance of making a profit depending on their safety net from crop insurance and the farm program. And hedging could increase those odds even more.

To be sure, beans so far in 2023 are following the down trending pattern seen in years of normal markets. But the fickleness of the notoriously unpredictable commodity cuts both ways: Surprises aren’t preordained to be bearish, improving odds for success.

Last week I detailed results of a “Monte Carlo” simulation that showed new crop corn hedges looked profitable. Soybeans appear to have just as good, if not even better potential.

These simulations look at thousands of different ways the market could play out during the growing season, based on yield patterns going back to 1950 that include variations to account for wide differences between what happens to individual producers in a given area and the country as a whole. As with corn, some growers do much better or much worse than the average, complicating the analysis.

Soybeans also offer a few twists from corn. Yields for corn historically can be both better and worse than soybeans. Since 1950 corn yields fell greater than 20% below normal more often than soybeans did, and corn also recorded more years when yields were 10% better than expected.

Demand for soybeans can also be more volatile. Corn is only starting to feel the influence of China and Brazil as major players. Good soybean crops from South America can swamp the world with too much supply, while China’s appetite for imports from the U.S. varies with political and economic winds.

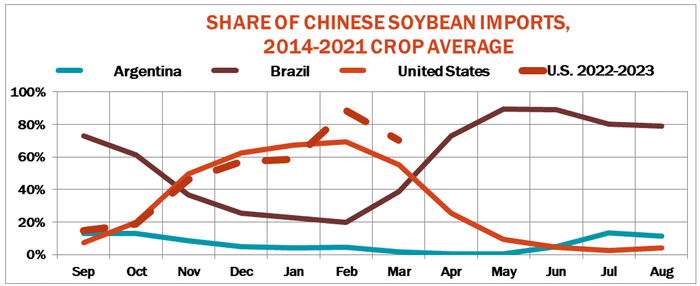

This makes forecasting 2023 prices even more uncertain than usual. The reopening of China from COVID lockdowns spurred a surge in buying soybeans from the U.S. that lasted longer than normal due to a delayed harvest in Brazil. U.S. originations accounted for 79% of Chinese imports in February and March, 11% more than average. But U.S. sales are slowing and some cheap Brazilian beans are even finding their way to U.S. crushers.

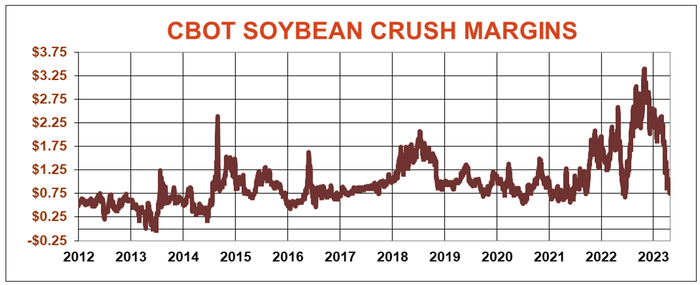

How many beans processors uses typically don’t vary as much from one year to the next as exports do. But hopes for a biodiesel boom make this component of demand unpredictable as well. Though year-to-date crush is still slightly below levels from the 2021-2022 marketing year, March crush posted by members of the National Oilseed Processors Association was the second highest ever for any individual month.

Strong crush margins likely convinced those operations to increase output. But margins plummeted in April, falling 75% from levels planted enjoyed at harvest in 2022.

Total U.S. soybean demand normally varies with the size of crops both here and around the world. Production looks ready to rise in South America, though those harvests are still a year off. Chinese economic growth, long a harbinger for its imports, remains unpredictable with demand also affected by an aging and shrinking population that’s no longer the biggest in the world – India is believed to have won that title.

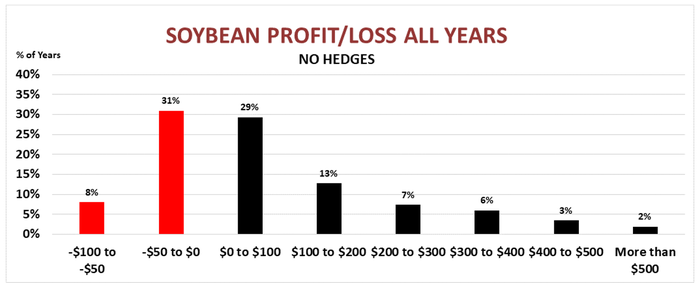

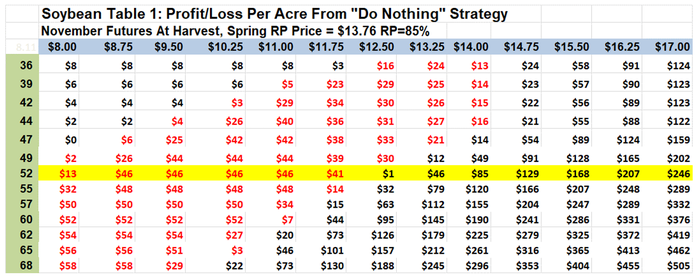

Even factoring in all this uncertainty, my historical simulations suggests hope. Growers who signed up for 85% Revenue Protection crop insurance and chose ARC for their government program option earned a profit in 61% of the time. As with corn, average profit of $81 an acre was distorted by high-income years with big rallies and/or bumper yields. The median profit was lower, around $7.

The “what if” sensitivity analysis prepared by the Excel spreadsheet Data Table function shows profit or loss produced by different combinations of harvest futures prices and yields. It includes opportunity for both red and black ink. But if revenues nosedive enough with low prices and low yields, safety nets could bounce returns back into black thanks to ARC and RP payments.

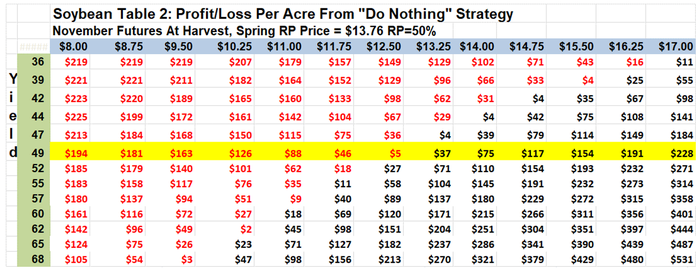

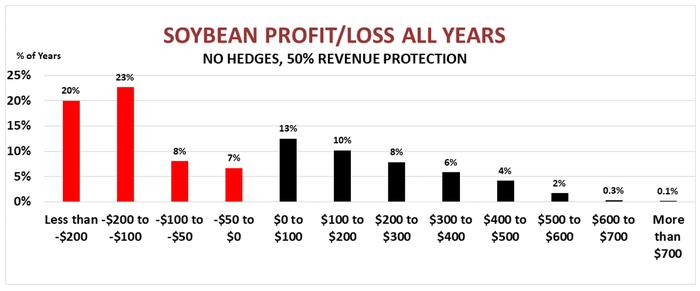

Some growers don’t pay up for 85% RP coverage because costs can be quite high. But the $13.76 spring price is close to a guaranteed profit for those who chose the highest election. Farmers who went on the cheap could be at risk. When the lowest RP level at 50% was plugged into the simulation, growers earned a profit in only 43% of the years. Earnings were again skewed due to some very boom years, so the average profit was $3 per acre. But the median was a loss of $53, with some very deep red ink possible when both prices and yields plummeted.

The warming of the equatorial Pacific, which likely is already underway, has a big impact on corn, producing yields averaging 5% above expected due to relatively mild summers with normal to above normal rainfall. The corn simulation based on years with El Nino summers was profitable just 37% of the time.

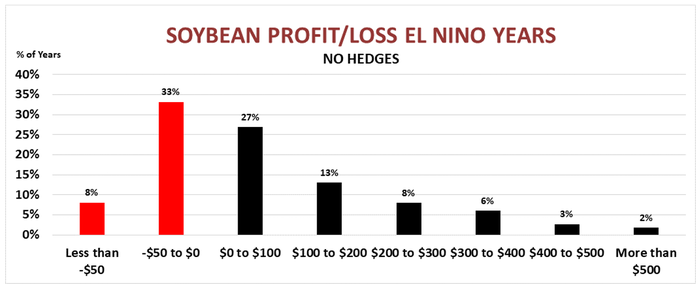

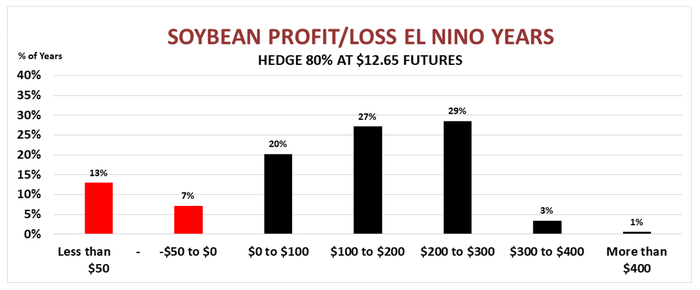

Soybeans fared better in years with the phenomenon. The simulation was profitable 59% of the time, only slightly less than during all years from 1950 to 2022.

Those results came despite, or perhaps because, soybean yields in years with El Nino summers lagged corn’s performance. They average around 2% above normal and were above normal less frequently too. Growers netted red ink in years with the worst soybean yields, when losses were even greater than corn. But soybeans also saw fewer years with really big yields that tended to depress prices.

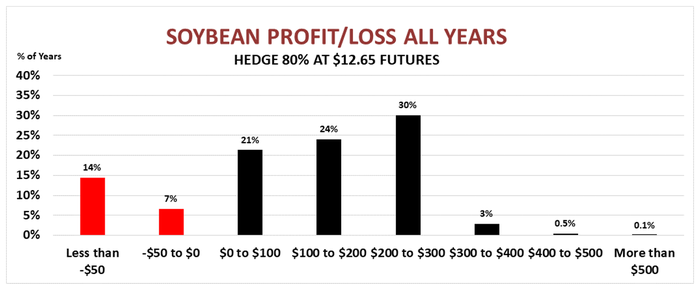

November futures may be down, but they’re not out. Even after the recent downturn on the board, hedging could be profitable. Plugging a $12.65 futures price available last week into these simulations produced a profit around 80% of the time, earning both average and median returns per acre topping $120. And that was true in years with and without El Nino summers since 1950.

Hedging doesn’t guarantee a profit – years with the worst yields still

produced losses and the red ink also flowed when really bumper crops confronted weaker than expected demand. But overall, laying off risk increased odds of success.

To be sure, rallies during the rest of spring and summer are possible – it’s around a 50-50 proposition historically. But further losses are also an alternative, and the biggest drops in down years topped $1 a bushel after May 1.

Marketing decisions are rarely easy. This year’s conditions suggest It’s a question of how much additional risk is worth waiting for a rally. Doing nothing in soybeans isn’t the worst choice for growers who can afford to wait. Taking some price risk off the table may be better for those who can’t.

Knorr writes from Chicago, Ill. Email him at [email protected].

The opinions of the author are not necessarily those of Farm Futures or Farm Progress.

You May Also Like

Current Conditions for

51°F

Partly Sunny

Day 52º

Night 36º

Enter a zip code to see the weather conditions for a different location.